What can retail learn from the past pandemics? Should we compare the Covid-19 Pandemic to the SARS Outbreak of 2002?

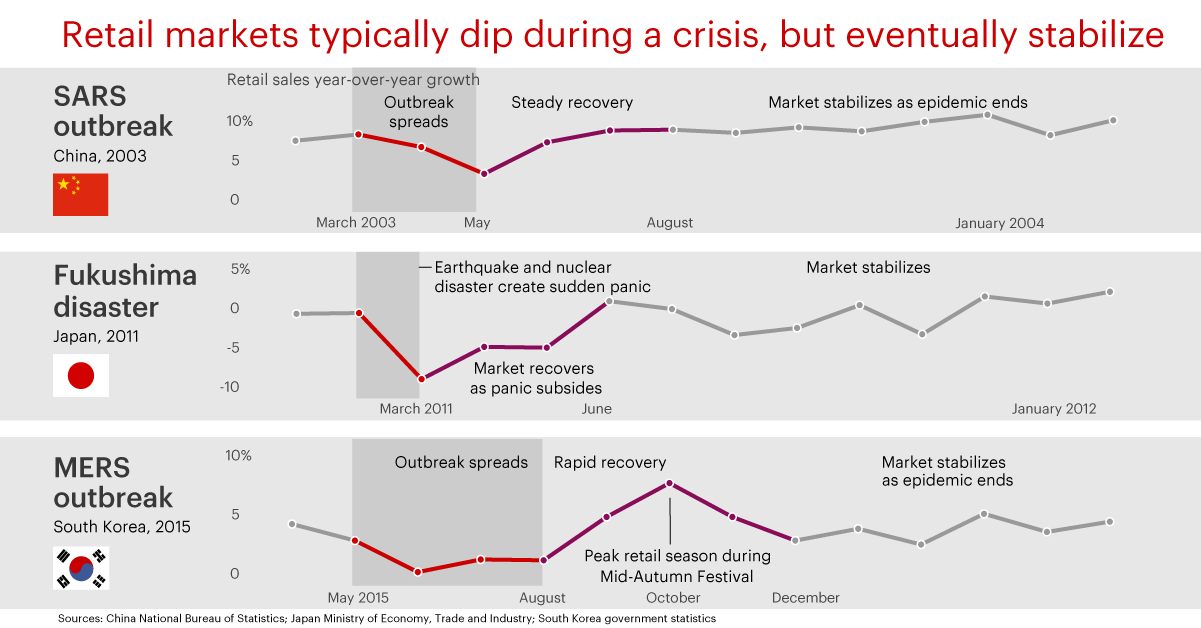

If we are to look at any past economic lockdowns due to viral outbreaks, it is quite clear that it takes an entire quarter for the market to recover into Business As Usual. But all of those outbreaks were limited in its geographical footprint and hence affected a limited number of cities and countries.

This time, it’s different.

We are talking about a full scale pandemic spread across the globe and has affected almost each and every country and market, retail included.

Source: Bain & Company

The only survivors who are barely hanging by their fingernails are FMCG especially the food and grocery sector, as they themselves are struggling with limited staffing, restricted transportation and absolutely broken supply chains. Now when we started working on this blog, we were expecting to find data that would reflect how each industry reacted to all of the past pandemics and plagues. We were wrong. What we did find though is repeated references to the SARS outbreak of November 2002.

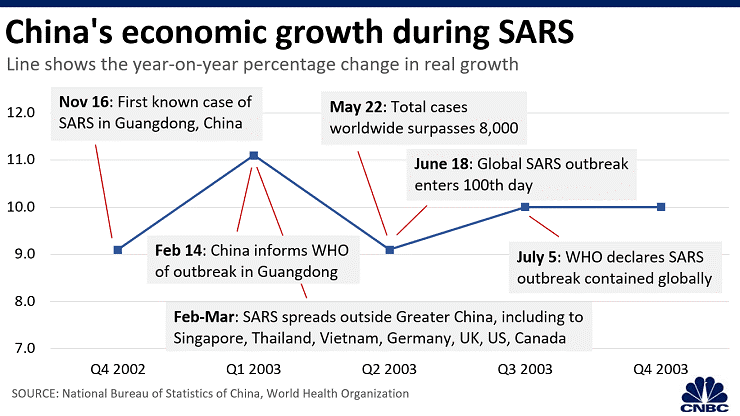

Now just to give you a little background, similar to the Covid-19 breakout, the SARS started in China in November 2002, but was not reported to the WHO until February next year. Between February and March the virus spread to the US, UK and Germany amongst others and the total cases reached around 9,000 with around 800 succumbing to the virus. Eventually WHO declared the outbreak to be contained by July 5th.

Source: CNBC

Source: CNBC

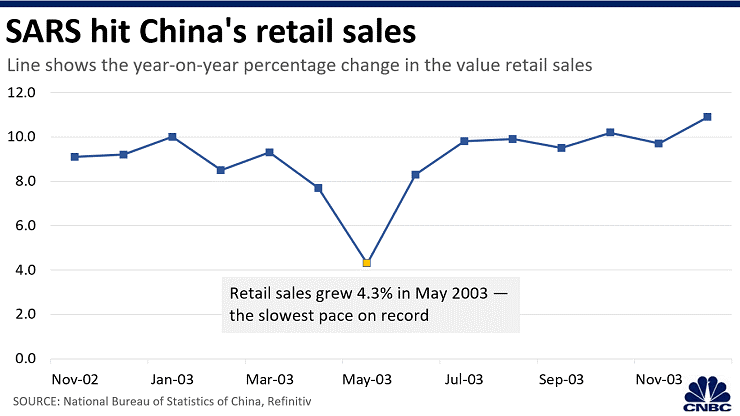

Just this scale of an outbreak caused the Chinese Retail market’s growth to halve during the same period; and remember, this was during the Chinese GDP’s upswing, which meant that they, in a way, got off easy back then with their overall growth rebounding in the following months to register an annual growth rate of 10% which was still better than their previous year’s 9.1%. That being said, some estimates showed that China’s annual growth in 2003 could have been half to 1 percentage points higher without the whole SARS disruptions.

Source: CNBC

Source: CNBC

It is also worth noting that this was the year the US attacked Iraq and got hold of Saddam Hussain. So the world’s attention was caught up mostly with those events while it recovered from the SARS situation. To us, right now, these numbers seem pale compared to the quantum of cases that we have witnessed so far and we have barely crossed half of April. As of today we already have more than 23 Lakh cases and 1.6 Lakh deaths globally.

And these cases are also distributed amongst the largest nations in terms of economy and geography this time around, which means the disruption is dangerously close to a recession, if not a depression. Due to the very expansive coverage of this pandemic, not only have the manufacturing hubs disrupted, but so have the supply chains. This chain of actions is exposing a ripple effect across industries, which is why this pandemic is unlike anything we have seen or experienced even on a miniature scale.

A model example for this is in the FMCG sector and its struggles right now.

Corporations are increasingly understanding the value of local sourcing, e-commerce enablement, omnichannel and community relationships. We are looking forward to taking a close look at each of these aspects in our upcoming blogs, so you can consider bookmarking our website.

From what we see right now, the worst hit strata of the society are the lower or working class. The people who live on wages are hardly the target market for organised retail. It is the middle class and upper middle class that matter the most to retailers and even the government. Also, did you know that “The Indian middle class constitutes 40 million or 3% of the population”. So instinctively, it is this 40 million or 4 Crore people that are the primary targets of established brands with urban and suburban presence.

Now while it’s true that most named corporations are trying very hard to not deduct pay, I have personally seen small and local brands cutting salaries in tranches like these wherein the founders/directors are not taking any pay at all:

While this helps for survival, the model is also reducing the purchasing power of your target consumer. Meaning not only will people be mentally exhausted post lockdown, but will also be cash strapped. It will be difficult for humans to shake off the habit of purchasing only essentials, and in some cases forced by their wallets to do so. We believe that in this time, the “true value” of a product will be reevaluated in the consumer psyche. The purchases could be more value driven than instinct driven.

While this helps for survival, the model is also reducing the purchasing power of your target consumer. Meaning not only will people be mentally exhausted post lockdown, but will also be cash strapped. It will be difficult for humans to shake off the habit of purchasing only essentials, and in some cases forced by their wallets to do so. We believe that in this time, the “true value” of a product will be reevaluated in the consumer psyche. The purchases could be more value driven than instinct driven.

Now don’t get me wrong, that does not mean people will go for cheap. (We have already seen the difference between a normal sanitizer at the start of the lockdown and literally watered down versions by the end of the first 15 days.). But people will be more careful about quality and longevity. This means that we as brands need to focus on the NEED part of our products and instead of the WANT. We will need to look at recategorizing our products and have utilitarian focused marketing wherever we can. This will reaffirm the purchase in consumers’ mind as not being wasteful.

In other cases, especially luxury items or lifestyle experiences, we can have the focus on ‘forgetting the lockdown’, but do make sure you do it carefully. You do not want to trigger their PTSD of the event. It will have long term effects on your brand perception. Make sure your brand doesn’t get too desperate in using the lockdown/curfew/quarantine bandwagon and wind up leaving a bitter taste in the consumer’s minds. We have a feeling that the luxury and ultra luxury market might even see a sharp uptick, but more on that in our next blog.

Stay Home, Stay Safe.

Quick Tip: Since consumers will have dipped into their savings, it is time that you reconnect with your banker to get more Credit Card offers with zero interest EMI to encourage purchases. It’s now or never.